Rahul had two objectives when he received a job offer in Bangalore: he wanted to purchase a home close to his new workplace and furnish it in a month. The catch? He was unsure if a personal loan could fill the gap or if a property loan alone would be adequate. Similar to Rahul, thousands of borrowers deal with this twin-loan conundrum every day.

Do you take out a home loan for a valuable item and make long-term EMI payments? Or do you take out a personal loan, which is more expensive but has a quicker disbursement and no end-use restrictions? The choice isn’t always clear-cut, depending on your timeframe, financial security, interest rates, and the objective you’re attempting to accomplish.

When considering a personal loan vs home loan, this blog will explain the differences between home loans and personal loans, compare the numbers, explain usage cases, and provide the most important answer: which is better for you right now, a home loan or a personal loan?

Understanding Personal Loans

A personal loan is an unsecured credit facility offered by financial institutions that allows borrowers to access funds without pledging any collateral. Medical emergencies, schooling, travel, wedding costs, and small home improvements are just a few of the uses for these loans. Personal loans have shorter payback terms and comparatively higher interest rates because there is no security involved.

Key Features of Personal Loans

- Loan Purpose: Flexible usage (weddings, travel, medical, home repairs, etc.)

- Loan Amount: Typically ranges from ₹50,000 to ₹40 lakhs, depending on income and credit profile.

- Interest Rate: Generally ranges from 10% to 24% per annum.

- Tenure: Usually between 1 to 5 years.

- Collateral Requirement: Not required.

- Processing Time: Fast disbursal, often within 48–72 hours.

Eligibility Criteria

Income level, work position, credit score (ideally 700+), and ability to repay are the main factors that determine eligibility. Lenders carefully consider the borrower’s financial situation because there is no collateral.

Understanding Home Loans

A home loan is a type of secured loan intended exclusively for the purchase, construction, or remodelling of residential real estate. The loan’s collateral is the property for which it is obtained. Home loans provide more advantageous terms, such as lower interest rates and longer repayment periods, because the lender bears less risk.

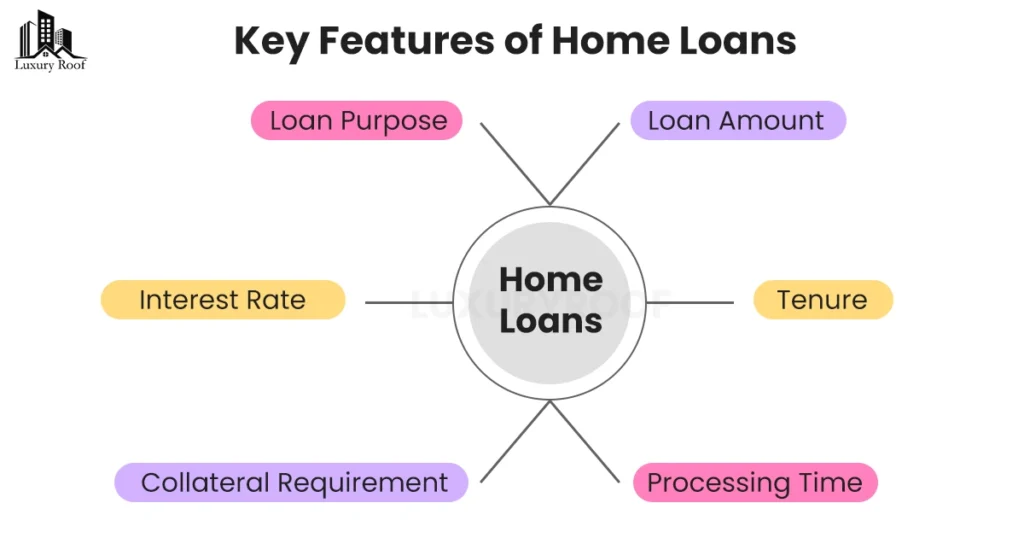

Key Features of Home Loans

- Loan Purpose: Purchase of a new house, construction, home improvement, or home extension

- Loan Amount: Based on the value of the property and repayment capacity (can go up to ₹5 crores or more)

- Interest Rate: Typically ranges from 8% to 10.5% per annum

- Tenure: Can extend up to 30 years

- Collateral Requirement: Mandatory (usually the house/property itself)

- Processing Time: Can take 7 to 15 days, depending on documentation and legal verifications

Eligibility Criteria

The value of the property being financed, the borrower’s age, income, employment stability, and credit score are all evaluated by lenders. It is also possible to increase loan eligibility by adding co-applicants, such as spouses.

Personal Loan vs Home Loan Interest Rate: A Financial Comparison

The interest rate is one of the most important factors separating these two loan kinds. Home loans have lower interest rates since they are less risky for the lender because they are backed by collateral. Because they are unsecured, personal loans are riskier and therefore have higher interest rates.

- Interest rates on home loans are typically between 8% and 10.5% annually.

- Interest rates on personal loans range from 10% to 24% annually.

Over time, this difference has a direct effect on the Equated Monthly Installment (EMI) burden and the overall cost of borrowing. Therefore, to make an informed financial decision, it is essential to comprehend the interest rate comparison between personal loans and house loans.

Difference Between Home Loan and Personal Loan: A Tabular Overview

To better understand the contrasting features of the two loan types, here’s a side-by-side comparison:

| Feature | Home Loan | Personal Loan |

| Purpose | Purchase, construction, or renovation | Any personal financial requirement |

| Collateral Requirement | Yes (secured against property) | No (unsecured) |

| Loan Amount | Higher (up to ₹5 crores or more) | Lower (up to ₹40 lakhs) |

| Interest Rate | Lower (8–10.5% p.a.) | Higher (10–24% p.a.) |

| Tenure | Long-term (up to 30 years) | Short-term (1–5 years) |

| Tax Benefits | Available under Sections 80C & 24(b) | Not applicable |

| Processing Time | Longer (7–15 days) | Quicker (2–3 days) |

| EMI Burden | Lower due to longer tenure | Higher due to short tenure and high rates |

Home Loan or Personal Loan: Which is Better?

The choice between the two depends on the purpose of the loan, repayment capacity, and urgency of funds.

Opt for a Home Loan if:

- You are planning to buy or construct a residential property

- You are eligible for tax benefits under Section 80c and Section 24

- You seek a lower interest rate and a longer repayment period

- You are comfortable pledging property as security.

Choose a Personal Loan if:

- You require funds for non-property-related expenses such as weddings, travel, or medical needs.

- You want quick disbursal without the hassle of extensive paperwork.

- You are not in a position to provide any collateral.

- The required amount is relatively small and short-term.

Therefore, the borrower’s unique needs and financial situation play a major role in determining whether a home loan or personal loan is preferable.

Tax Benefits: A Home Loan Advantage

Another crucial area where home loans have an edge is taxation. The Indian Income Tax Act offers various tax deductions on home loans:

- Section 80C: Deduction up to ₹1.5 lakh on principal repayment.

- Section 24(b): Deduction up to ₹2 lakh on interest payment.

- Section 80ee/EEA: Additional deduction for first-time homebuyers under certain conditions.

However, unless the borrowed funds are utilized for home improvement or commercial activities, in which case there may be some exceptions, personal loans typically do not provide any tax advantages.

Which Loan Should You Choose?

In the end, choosing between a home loan and a personal loan should be determined by

- Nature of the requirement: Is it a general necessity, or is it connected to property?

- Loan amount: Home loans are a preferable option for large purchases.

- Repayment capacity: Longer-term, lower EMIs might be more manageable.

- Collateral availability: You can access reduced loan rates if you have real estate to pledge.

- Need for tax planning: Tax preparation is necessary since home loans can be used as a tax-saving tool.

A personal loan is suitable if the need is short-term, urgent, and does not entail purchasing or improving real estate. However, a home loan is nearly always the preferred choice for long-term, structured housing needs.

Summing Up

Personal loans and home loans are both significant financial instruments with distinct functions. Home loans offer a cost-effective path to property ownership, replete with tax advantages and structured repayment alternatives, while personal loans offer flexibility and rapid access to funds.

When evaluating personal loan vs home loan options, borrowers can make well-informed decisions that support their long-term financial goals by carefully weighing the distinctions between home and personal loans, interest rates, tenures, and eligibility restrictions.

In conclusion, having a solid grasp of the differences between home and personal loans guarantees that you will not only reach your short-term financial objectives but also preserve your long-term financial security.